10 Steps to Build Your Pipeline & Close More Loans |

May.11 |

By Todd Duncan

Since 1992, I have studied the strategies and behaviors of top producing Loan Officers throughout America. I have personally interviewed over 800 loan officers that make at least $250,000 a year in sales commissions, work less than 50 hours a week, and have an approach to achieving balance in their life. RJ Crosby comes to mind, and just last year he called to thank me because he had “closed 45 loans in one month and had taken two weeks off.” Mike Metz texted me that he had “closed 125 loans in the last two months and grossed over $550,000 in revenue. That’s the kind of success I’m talking about.

What do Loan Officers like RJ and Mike do to get to that level? And if you knew their secrets, you could model those and get the same results. At Sales Mastery every year, Loan Officers do exactly that – showcase their “secrets”, which are not really secrets, but truths, laws, principles, that when followed make the biggest difference in your life and your business.

Here are the 10 steps that I teach that I guarantee will help you build your pipeline, close more loans, and give you the best year ever.

1. Operate From a Plan

I have been teaching this for years, and in fact the plan that I think sets you apart from your competition and would allow for you to build great wealth is the same plan I used to do exactly that over 25 years ago. I call it the Magic Formula. It’s straightforward and looks like this. Get 10 Referral Partners, like a Realtor, to refer you 8 borrowers a month each that will buy a home in the next 12-months.

If you master the borrower conversation and have strategic referral synergy with your partners, you will convert 25% to applications that month. So, if you talk to 80, you get 20 loans apps. If 90% of those close, you close over 200 loans a year and you are in the top 1% of Loan Officers in America. And by the way, if your conversion rate goes to 75%, which is where the pros are, that is over 600 loans a year. Think of that business plan at a couple thousand a loan and you could get really excited I’m sure.

2. Prospect and Set Appointments with Referral Partner Targets

The number one avoided success discipline is prospecting – no question. Loan officers are locked in the grip of fear when it comes to prospecting. Why? Because they have not achieved greatness in the area of making sales calls. This was the first thing I got good at and I had a 90% close rate of calls to appointments to relationships.

Every business needs customers, and while you can find buyers today through lead machines like Zillow, or radio shows, those consumer direct approaches have high volume, which is a time consumer, and low conversion, which is poor ROI.

Nothing wrong with either or any approach as long as your time is leveraged and your conversion rates are high. I have found the best way to do this is through one to one relationships, where the referral is strong to you, the conversion is high and the ROI is maximized.

So, you have to get good at partnering, especially if you know your financial dreams can come true with only 10 solid partners. The best way to find, for example, new real estate agents is on every deal you have. Simply work all sides to the transaction and you can set appointments with any agent or affinity partner involved. As you continue reading, you will see how to do this.

3. Ask Strategic Questions to Foster Trust and Learn Opportunities to Add Value

When you have an appointment set, it’s important to ask meaningful, well thought out questions. You cannot have strategic partnerships unless you guys are talking about strategy. And you can’t talk about strategy without uncovering needs. And you can’t uncover needs unless you ask questions.

When you ask the right questions you get the insight to what the prospect needs from you for their business to operate at a higher level. To be a “strategic” partner, you must help develop strategy around these needs and you will secure the relationship forever.

4. Systematic Follow-Up:

Weekly with Partners

Here’s a rule I live by: if you are not in touch you are out of touch. If you don’t connect with your partners on a weekly systematic basis, you will not optimize the growth the partnership has to offer. And, you will not develop the habit of securing the leads that can come out of the relationship through a more consistent approach.

Remember your plan. If you need two borrowers a week to speak with, you must ask for them.

Weekly with Borrowers

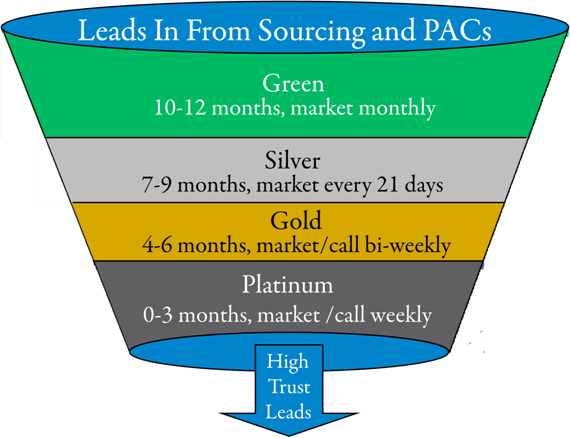

Another critical rule I call “The Nine Magic Words” – If you don’t follow-up, they won’t follow-through. Personally, I love the idea of “Catch and Release” as a fishing protocol. I love throwing trout back into the stream and I love tagging a large Marlin and letting it go. But, catch and release is a horrible business strategy. The most successful loan officers break borrowers into four categories and stay in touch with them until they apply – which some will do immediately, so might do after talking to other lenders, some might do after thinking it over, and some might do after months of contemplation.

The key is you want to be right there, having already established trust, when they decide to pull the trigger. SIT stands for Stay In Touch and you cannot go wrong using the below diagram and your CRM to continue to add value to your borrower prospects and increase your conversion over time.

Regularly with Closed Customers

Here’s another important rule – If you want your clients for life, you must talk to them during their life.

Far, far too often loan officers do not have a dialed in retention strategy for their closed loan borrowers. This is the most valuable part of your database in that it represents your annuity income. It is the true economic value of your labor to this point in your career. To leverage that, you must be in touch.

If one buyer can do another loan with you and refer you to three others over the next 5 years, that’s 4 loans, or about $8,000 in commissions. What if you have 400 of those buyers? That’s $3,200,000 over five years. That’s $640,000 a year! This is a whopping $53,300 a month! Do I have your attention? All you have to do every year is:

1. One annual review

2. Four quarterly calls

3. 6-10 meaningful marketing touches

5. Pipeline Efficiency: The Perfect Loan Application

There was a wonderful book written in the mid-nineties by Jeffrey Meyer entitled, If You Can’t Find the Time To Do It Right, When Will You Find The Time To Do It Over? I have been instructing loan officers for a very long time on the importance of having a huge commitment to quality in their loan applications.

The mindset of the top producer is the loan application must be complete. It must have all documents needed to support qualifying for the loan. It must have a cover letter to let processing and underwriting see what the Loan Officer sees. And, it will be approved. The top producer never “Hopes” a loan will get approved.

In Stephen Covey’s book, The Seven Habits of Highly Effective People, my favorite habit is Be Proactive. It solves 99% of your daily problems around loan file and pipeline management. This is by far the most important efficiency habit you can ever develop. Always remember that bad loans will always get worse and good loans will rarely get better. You can be PROACTIVE on bad loans, but it is still a less effective approach.

6. Pipeline Efficiency: Proactive Communication Standards

Another great efficiency rule - If you don’t call them, they will call you. The perfect pipeline management system is the one that eliminates all inbound calls from all parties to a transaction for the duration of the processing and closing of the loan.

What is your communication system for your pipeline? As of the end of last year, well over 50% of a loan officer’s time goes to reacting to loans in process – the opposite of proactive. In a nutshell, here’s RJ Crosby’s system. And by the way, their phone doesn’t ever ring except for new buyers…. What a concept!

1. Weekly pipeline review meeting with team at 2:30. ALL status is emailed out by 5:30 to ALL parties to the transaction. Since they all expect it on Monday, they do not call the office.

2. Morning huddles for 15-minutes reviewing all pipeline movement for the day. What loans have action on them today?

3. Based on #2 above, RJ then calls the listing agent, the selling agent and the buyer and advises on loan movement. He measures 4 milestones – Submitted, Appraisal in, Docs Out and Funded. Since everyone knows, including the borrower, that this is the system, it is rare that he receives inbound calls.

4. As promised on Number 2 above, RJ then uses every opportunity to connect at funding with every agent he does not do business with regularly and sets an appointment to do Number 3 above to initiate a new relationship to expand his business.

The single most important thing I would do if were in business today would be this – everything success, rises and falls on your efficiency.

7. Customer Survey’s

This is huge and one that too many loan officers shy away from. We all want to serve the customer well. At least I hope that is an assumption I can make. However, we usually don’t have a system in place to make sure this is happening, except after closing, which is too late.

All loan officers should survey their borrowers:

24-hours post application: make sure everything is working so far! Answer any questions.

Mid-process: halfway through the transaction – are we on track?

72-hours post-closing: how did we do? Will you use me again? Who do you know?

It is impossible to exceed a customer’s expectations without knowing what those expectations are, so make sure you are asking the right questions, you know how they’d like to be communicated with and how, you know the best times to reach them, you know their service expectations, etc.

And, ALWAYS survey your referral partners, and do it weekly – “do you have any needs I need to meet or meet better?”

RULE – Never run from a customer, always run to them.

8. Pre-closing Reviews

This is one of the best strategies ever invented in terms of loan file efficiency and eliminating problems at closing. First of all, most loan officers spend too much time at the end trying to make up for everything that did not go right at the start. Assuming you are implementing the rest of the tips shared with you so far, the pre-closing review is a natural extension of your commitment to quality and service.

It can happen between 3 and 7 days from closing and essentially is the final checklist on the “runway” to closing the loan. On this call you are confirming the closing date, location, directions, loan terms, final needs, and all the essentials that a borrower needs to know to make closing smooth.

In the old-days going to closing was a great idea. But as your volume builds, that is harder to do plus if there was a problem, it was hard to fix it then. So, again, DO IT RIGHT THE FIRST time is what the Pre-Closing Review strategy is all about.

9. Build a Team and Delegate Everything

No question on this one. I will be bold and come out straight away and tell you that 80-90% of what you are doing every day does not produce income for you, including email. I will tell you with 100% certainty that if you don’t have an assistant you are one. And, I will go so far as to say that if you don’t build a team of 1-5 people around you and this is your career, you will take on average 4-6 times longer to produce your optimum results – let’s see – what does that look like – well, maybe you take 40 years to do what you could have done in 10!

10. Say Thank You

And make your thank you huge and memorable! I recently interviewed Harvey McKay who without doubt is one of the best business writers of our time. The interview was on his most recent book, The McKay MBA of Selling. The next day, I got an overnight FedEx and inside was a 5-page thank you letter. Yes, five pages of this:

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

Thank You! Thank You! Thank You! Thank You! Thank You! Thank You!

That’s right. Over 600 thank you’s for a 45-minute interview. And then a simple closing paragraph of his deep appreciation for our time together. How you say thank you is as important as saying thank you. Make your thank you as memorable as you can and business will always flow your way.

comments powered by Disqus Follow me on Twitter

Follow me on Twitter Like me on Facebook

Like me on Facebook  Connect on LinkedIn

Connect on LinkedIn